Tax System in India

The Tax System in India is mainly structured by the Central Government and State Governments. Some minor taxes are also imposed by the local authorities such as the Municipality and the Local Administration. The tax rates in India are decided by considering the income of people, economic activities in that region, locality, etc. The government also provides subsidies to poor people who cannot pay more taxes. You can download the Tax System PDF from the official sources of the administration. The Tax System PDF contains the tax rates and all other details of the tax.

Tax System

Tax System refers to the set of rules, policies, and norms followed to collect the tax on various commodities. The Tax system contains the guidelines and instructions implemented by the government authorities. The tax system of the country is responsible for the economic growth and financial stability of the country. So the countries decided on their tax system by considering all the terms for their economic growth. The tax rates are decided by the financial authorities and government and they may differ from one another. Refer to this article to know all the terms and concepts of the tax system.

Tax System Meaning and Classification

The tax system is the system in which tax is decided for various purposes. The tax system enhances the economic growth of the nation. So the citizens and students must know the tax system’s meaning and understand its related terms well.

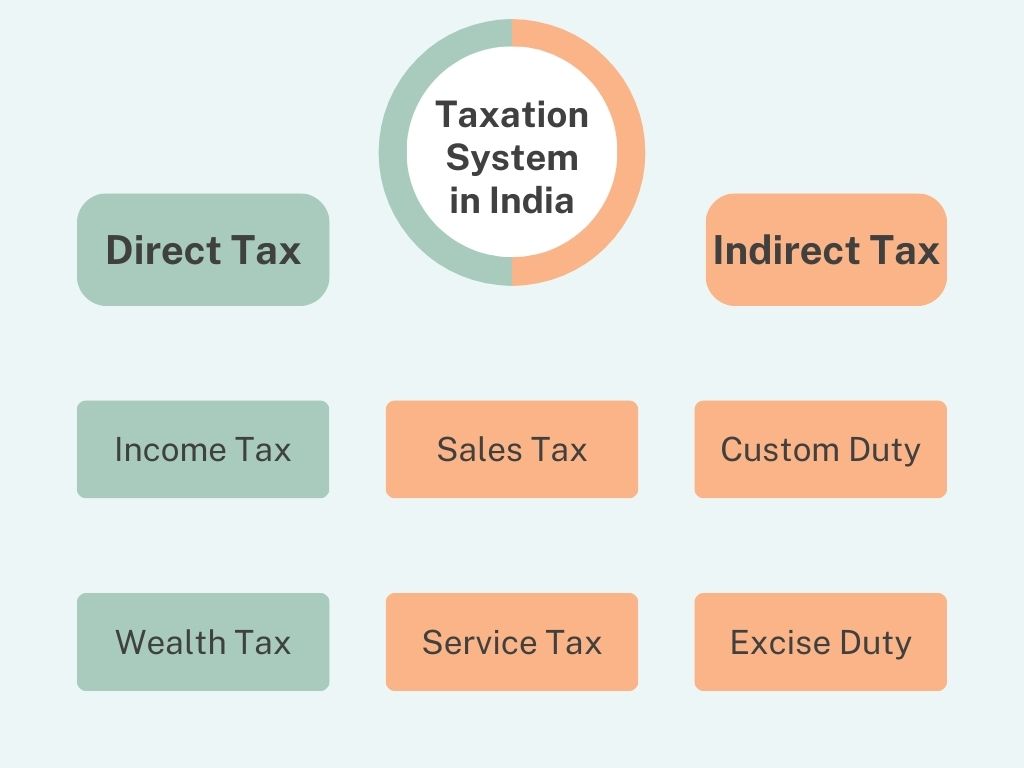

The taxes are classified mainly into two types viz. Direct Tax and Indirect Tax. Both these taxes are discussed here in detail.

I. Direct Tax

The taxes are paid directly by the individuals to the tax authority or Government or the organization which charged them. A taxpayer pays a direct tax to a government for different motives, including property tax, income tax or taxes on assets, FBT, Gift Tax, Estate Tax, Capital Gains Tax, etc. In India, the Central Board of Direct Taxes (CBDT) deals with tax-related issues and the formulation of taxes.

II. Indirect Tax

The taxes are charged to the individual indirectly and they need to bear it. The indirect taxes include Sales tax, Excise tax, Value Added Tax (VAT), Goods and Service Tax (GST), and other specific taxes. The indirect taxes are to be paid to the retailer or the businessman.

Tax Rate Long-Term Capital Gains

Tax Rates are responsible for the long-term capital gain of the country. The long-term capital gain can be calculated using the formula given here. Long-term capital gain = Final Sale Price – (indexed cost of acquisition + indexed cost of improvement + cost of transfer), where: Indexed cost of acquisition = cost of acquisition x (cost inflation index of the year of transfer/cost inflation index of the year of acquisition).

Tax Rates Income

The tax rates are formulated based on the income of the people. The tax rates are changed from time to time. You can check the tax rates under different Income Tax Slabs for both Old Tax Regime and New Tax Regime. The New Tax Regime came into effect from 01 April 2023 for income earned between 2023-24 and onwards.

| Tax Rates for Different Income Tax Slabs in India | |||

| Old Tax Regime | |||

| Income Tax Slab | Indian Residents (<60 years) | Resident Senior Citizens (≥60 and ≤80 years) | Resident Super Senior Citizens (>80 years) |

| Up to Rs.2.5 lakh | Nil | Nil | Nil |

| Above Rs.2.50 – Rs.3 lakh | 5% | Nil | Nil |

| Above Rs. 3 lakh – Rs.5 lakh | 5% | 5% | Nil |

| Above Rs. 5 lakh – Rs. 10 lakh | 20% | 20% | 20% |

| Above Rs.10 lakh | 30% | 30% | 30% |

| New Tax Regime | |||

| Up to Rs. 3 lakh | Nil | ||

| Above Rs. 3 – Rs. 6 lakh | 5% (Tax rebate u/s 87A) | ||

| Above Rs. 6 lakh – Rs. 9 lakh | 10% (Tax rebate u/s 87A up to Rs. 7 lakh) | ||

| Above Rs. 9 lakh – Rs. 12 lakh | 15% | ||

| Above Rs. 12 lakh – Rs. 15 lakh | 20% | ||

| Above Rs. 15 lakh | 30% | ||

Tax System Before GST

With the implementation of Goods and Service Tax (GST) in India, lots of differences and changes are observed in the tax system as compared to the tax system before GST.

We all have heard that GST will become cheaper. The real notion is that GST will help ‘considerably’ remove the ‘cascading effect’ of taxes, a problem that is deep-rooted in the old system.

The Cascading effect of taxes indicates the tax on the tax system. In the old tax system, for example, suppose a commodity of Rs 100 after charging 10% tax becomes Rs 110, further (say) 10% CST (central sales tax) is levied not on 100 but 110 making the total price of the commodity 121 i.e 110+11=121. The GST practically eradicates this problem.

The second major difference is that GST is a ‘DESTINATION BASED’ tax or consumption-based tax.

It means if goods are produced in Gujarat and consumed in Tamil Nadu then the tax revenue so generated goes to the TN govt which was not the case with the old system in which the government of that state earned the tax revenue in which goods were produced or manufactured.

Unlike the old tax system, GST is simpler with only four tax slabs i.e. 5%, 12%, 18%, and 28%.

In the old system, there were no provisions for e-commerce websites but in GST there is a defined treatment for e-commerce platforms.

GST facilitates transparency as most of the procedure is online with defined formats that have to be simply filled.

Components of GST

The GST has many components which are listed below.

CGST – Central GST, applicable on supplies within the state. A tax collected will be shared with the Central Government.

SGST – State GST, applicable on supplies of goods within the state. A tax collected will be shared with the State Government.

UTGST – Union Territory GST, applicable on supplies within the union territory. A tax amount collected will be shared with the State/UT.

IGST – Integrated GST, applicable on interstate transactions. Tax collected is shared between the Central and State governments.

Tax System In the Mauryan Empire

The tax system in the Mauryan empire was formulated by Kautilya’s Arthashastra. Land revenue was the main source of income and the other sources of taxation were forests, mines, customs, trade, and crafts in the Mauryan Empire.

The tax was 1/6 of the production of the peasants as the royal share. The state also received 1/4 and sometimes 1/2 from the sharecroppers who received land and other agricultural inputs from it. The peasants also paid another tax known as the pindakara, imposed on the groups of many villages.

This tax system assisted the government in further developing the monarchy by using this money to pay salaries, maintain armies, and for the welfare of the people.

Also Read:

Upcoming Government Exams, Complete Govt...

Upcoming Government Exams, Complete Govt...

Govt Jobs 2025, Latest Upcoming Governme...

Govt Jobs 2025, Latest Upcoming Governme...

SSC Exam Calendar 2025–26 Out, Check A...

SSC Exam Calendar 2025–26 Out, Check A...